"An attempt to remedy the consequences of a distortionary policy with another distortionary policy"

PJM’s new capacity market paper reveals a problem we have been avoiding for two decades

Source: Yet another productive conversation I had with ChatGPT.

PJM’s recent white paper, Powering Reliability Through Market Design, does not solve the problem underlying its title. But the paper is extremely valuable because it acknowledges that the foundational assumptions of organized capacity markets no longer fit the environment in which those markets operate, and does so more openly than most institutional discussion in this industry. That candor is significant.

The striking thing about the paper is how familiar the concerns are. Reading the document, I recognized the same institutional problems that were already visible nearly two decades ago during the early expansion of organized capacity mechanisms. In a chapter on resource adequacy and capacity markets in my 2009 book Deregulation, Innovation and Market Liberalization (Chapter 7), I argued that those mechanisms were emerging largely because organized wholesale markets had combined two institutional design choices that interacted badly: price caps and suppressed demand responsiveness. The resulting market structure then required administrative supply-side mechanisms to compensate for demand-side flexibility it had institutionally prevented from developing.

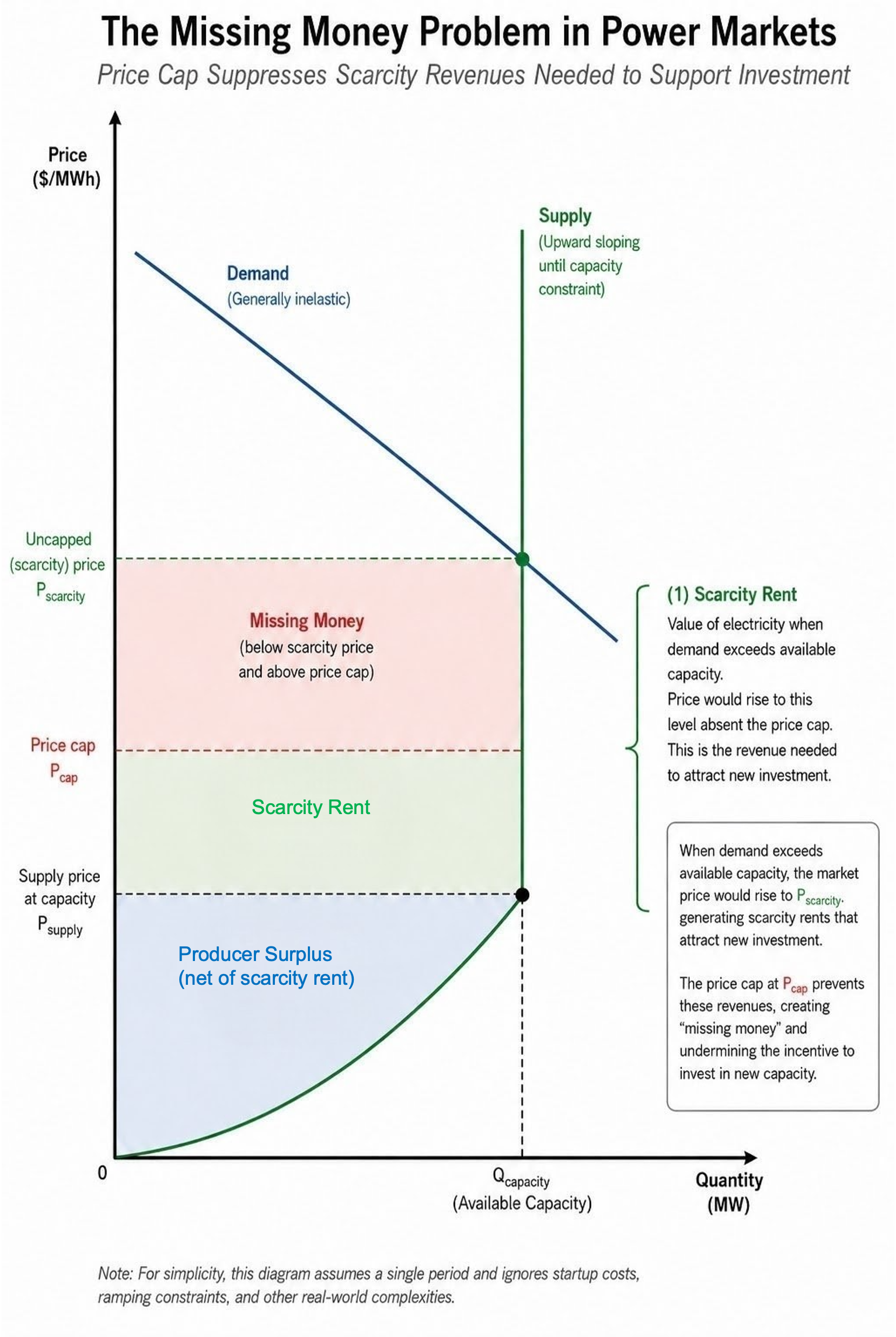

The Missing Money Problem Was Never Purely Technological

The conventional justification for capacity mechanisms is familiar. Electricity markets cap scarcity prices to mitigate market power and political backlash. Most retail customers face flat or quasi-flat retail rates rather than real-time prices. Demand therefore becomes highly inelastic precisely during scarcity conditions, limiting the ability of energy market revenues alone to support investment in resources needed primarily during peak reliability events. Capacity mechanisms emerge to supply the missing money — the revenue shortfall created by combining administrative price caps with inelastic retail demand.

This logic has long underpinned organized capacity mechanisms throughout wholesale power systems. But even in 2009, this explanation struck me as incomplete because it treated demand inelasticity as though it were an unavoidable technological characteristic of electricity systems rather than partly the consequence of institutional design choices. As I wrote then, capacity mechanisms are “an attempt to remedy the consequences of a distortionary policy with another distortionary policy.”

That framing remains central to understanding today’s resource adequacy debates.

Retail price caps, limited dynamic pricing, barriers to demand aggregation, insufficient integration between wholesale and retail markets, and governance structures designed around passive load all suppress the emergence of active demand participation. The resulting lack of demand elasticity creates the appearance that administrative supply-side procurement is necessary to maintain reliability; this appearance, though, is at least partly endogenous to the institutional architecture itself.

The irony is that organized markets have spent two decades building increasingly elaborate administrative mechanisms to compensate for the absence of demand responsiveness while simultaneously preserving many of the institutional arrangements that suppress demand responsiveness in the first place. PJM’s paper indirectly acknowledges this reality throughout. Its discussion of the credibility trap is especially illuminating: PJM correctly recognizes that scarcity pricing during tight conditions is economically rational, yet those same scarcity prices create political backlash because large portions of load remain exposed to volatility without corresponding flexibility or meaningful hedging arrangements. Policymakers then intervene, investors discount the credibility of future market revenues, investment becomes more hesitant, and scarcity persists. Lather, rinse, repeat.

This dynamic reveals a problem deeper than insufficient supply-side incentives: a broader institutional problem involving governance, risk allocation, and the persistent underdevelopment of active demand.

The Administrative Demand Curve as Epistemic Substitute

One of the most revealing features of organized capacity markets is their reliance on administrative demand curves. PJM, ISO-NE, and NYISO all eventually adopted downward-sloping administrative demand curves intended to approximate the value of future capacity resources. Yet the fundamental problem with these curves has always been that they substitute for actual preference revelation.

As I argued in 2009, “the artificial capacity product has no intrinsic value to customers,” because what customers actually value is reliability itself, not an engineering reserve margin target. The resulting administrative demand curves therefore become bureaucratic approximations of preferences that markets themselves are institutionally constrained from revealing directly. At best, such curves are rough estimates derived from incomplete information; at worst, they become bureaucratic substitutes for the decentralized discovery processes that active markets would otherwise facilitate.

My recent work on RTO governance argues that RTOs are best understood not simply as market operators but as governance institutions managing a congestible common-pool resource through rule-defined participation and exclusion. These institutions are non-replicable — no competing alternative can simply be constructed — meaning that the rules defining who participates, on what terms, and bearing what obligations become the primary margin of institutional adaptation rather than competitive pressure from outside.

That framing exposes a basic epistemic limitation: the distributed knowledge embedded in modern electricity systems — about flexibility, reliability preferences, and operational capabilities — is precisely what centralized administration struggles to incorporate, yet organized market governance still largely reflects the institutional assumptions of the 1990s restructuring era: centralized thermal generation, homogeneous demand, and limited customer participation. Administrative constructs increasingly substitute for the decentralized coordination they were never designed to replace.

Administrative demand curves substitute for actual demand expression, accreditation methodologies substitute for market discovery regarding reliability value, centralized reserve targets substitute for differentiated reliability preferences, and capacity constructs substitute for forward contractual coordination. The more technologically heterogeneous the system becomes, the more administratively demanding this substitution becomes, requiring more regulatory complexity to compensate for the coordination it cannot fully supply.

The Accreditation-Penalty Trap

Recent work by Ke Xin Zuo, Joshua Macey, and Jacob Mays identifies a structural dilemma at the institutional core of capacity market design. Capacity markets require non-performance penalties strong enough to create honest performance incentives, but penalties strong enough to be economically efficient expose suppliers to catastrophic financial risk when outages are correlated, as they were during Winter Storms Elliott and Uri. Under those conditions, high penalties drive generators toward default, and bankruptcy itself becomes a hedge against non-performance. Softening the penalties restores the problem they were designed to solve: suppliers again overstate their reliability contributions, and load again bears the consequences.

The institutional response has been to develop increasingly elaborate accreditation methodologies — marginal effective load carrying capacity (ELCC) estimates, performance assessment hours, seasonal accreditation — substituting regulatory constraints on position size for the market-based performance discipline that adequate penalties would otherwise provide. But accreditation introduces compounding challenges of its own. Optimal values depend on the resource mix at the time of the capacity auction, not the mix that will exist at delivery. Correlated outages are rare by design, making the hardest-to-model events the most consequential ones. And adopting improved methodologies requires navigating multi-veto stakeholder governance structures that move more slowly than the resource mix is changing.

The result is a mutually reinforcing administrative expansion: weak incentives require elaborate accreditation, elaborate accreditation requires complex governance, complex governance requires long implementation timelines, and long timelines mean that accreditation methods chronically lag the technical realities they are designed to measure.

PJM’s paper largely takes this institutional inheritance as given. Zuo, Macey, and Mays draw the more fundamental inference: reduce reliance on administrative accreditation by restoring economic incentives through stronger price signals in the energy and ancillary services markets, using accreditation primarily to assess credit risk rather than substituting for performance incentives that markets should supply directly. That inference maps directly onto PJM’s Path C proposal, as well as onto the vision of integrated spot and forward energy markets that I argued for in 2009.

Hedging, Risk Allocation, and the Architecture of Markets

Farhad Billimoria’s recent Substack article on hedging architectures reframes organized wholesale markets fundamentally as systems for allocating and managing risk rather than merely as systems for dispatching generation resources. That perspective clarifies what PJM’s three proposed pathways actually are: alternative hedging and risk-allocation architectures, not just alternative market designs. The Stabilized Markets pathway (Path A) relies more heavily on long-term centralized hedging structures, requiring load to be covered by forward commitments before the spot auction, preserving the capacity market while insulating consumers from its price volatility. Differential Reliability (Path B) reallocates reliability risk across customer classes or geographic areas, making explicit the allocation that currently happens implicitly and arbitrarily. The Energy Market Transition pathway (Path C) shifts revenue recovery toward the energy and ancillary services markets while relying on long-term energy contracting to provide the consumer protection that stable administrative capacity payments currently offer.

Billimoria correctly observes that no one-size-fits-all architecture exists; the appropriate design depends on regulatory structures, retail market development, and consumer engagement in each jurisdiction. This insight echoes arguments I advanced in 2009 about the importance of integrated spot and forward energy markets and the use of financial call options as transitional resource adequacy mechanisms — offering revenue certainty to investors while creating direct, market-based performance incentives rather than administrative ones (an idea I credit to the brilliant Shmuel Oren). Forward financial arrangements are constitutive of resource adequacy.

But even sophisticated discussions of hedging architectures like Farhad’s tend to understate one dimension: the importance of demand responsiveness itself. The problem is more than incomplete financial markets; it encompasses incomplete institutional participation. Technology increasingly enables active, flexible demand participation — smart devices, automated controls, distributed storage, EV charging, flexible industrial processes, and advanced metering all expanding the feasible scope of decentralized responsiveness — yet governance structures, retail rate design, participation rules, and market institutions still largely treat demand as passive load rather than as an active reliability resource, artificially inflating the scale of administrative procurement needed to compensate.

Differential Reliability and the Institutional Transition

Perhaps the most consequential element of PJM’s paper is its discussion of Differential Reliability — significant not primarily as an operational proposal but as an implicit acknowledgment that reliability preferences and operational capabilities are becoming irreversibly heterogeneous.

Some customers may value extremely high reliability and willingly pay for it, while others may prefer lower-cost service with greater exposure to curtailment or dynamic pricing. Some loads may be highly flexible and technologically capable of rapid adaptation (including the hyperscale data centers whose load growth is driving the current situation) while others remain relatively inflexible. This heterogeneity connects directly to arguments I made in 2009 regarding differentiated reliability products and the possibility of technology enabling what I called “privatizing many aspects of reliability”, drawing on the vital, seminal work on priority service of Chao and Wilson (1987).

Once differentiated reliability becomes institutionally feasible, the logic of administratively pooled uniform reliability begins to weaken. Demand no longer appears merely as passive load requiring protection through centralized reserve procurement. Instead, demand itself becomes an active reliability resource capable of dynamic adaptation in response to prices, contractual arrangements, and system conditions, changing the structure of the resource adequacy problem fundamentally. The central question becomes less about determining reserve margins administratively for undifferentiated passive demand and more about creating governance institutions enabling decentralized coordination among heterogeneous participants with differing capabilities, preferences, and risk tolerances. That governance transition is difficult, requiring changes in retail rate structures, market rules, legal obligations, property rights, and technology deployment. But the mounting strain visible in organized capacity markets suggests that avoiding this transition indefinitely may prove more difficult still.

A Bridge, Not a Destination

One argument from my earlier work seems especially relevant today: capacity mechanisms, if necessary at all, should function as transitional mechanisms rather than permanent fixtures, bridging toward more integrated spot and forward markets with active demand participation, clearer property rights, and richer forms of decentralized coordination. Specifically, I proposed that regulators stipulate milestone-based sunset provisions for capacity markets, reducing their scope as the volume of forward commitments in financial markets approaches the desired reserve margin.

That concern now appears even more pressing than it did then.

Administrative capacity mechanisms tend naturally toward institutional entrenchment, with entire business models, stakeholder coalitions, regulatory processes, and governance structures evolving around them, making the mechanism originally intended as a transitional response to incomplete market development into an obstacle to further institutional adaptation. As I said in 2009, imagine if 1850s law had dictated the existence in perpetuity of a capacity market for the production of whale oil. That deliberately provocative analogy has a serious underlying point: institutional resilience requires an ability of governance structures to evolve, adapt, and sometimes disappear as technologies and coordination mechanisms change.

PJM’s white paper represents an important step forward in acknowledging the depth of the current institutional strain, opening space for a more fundamental conversation than this industry has generally been willing to have.

The strain affecting organized wholesale markets arises both because generation investment has become more difficult and because the institutional framework continues suppressing decentralized demand responsiveness, differentiated reliability preference expression, dynamic coordination, and risk-sharing that modern technologies increasingly make feasible. Relaxing those suppressive institutional constraints — through retail rate reform, expanded demand participation pathways, clearer property rights, and milestone-based governance transitions — goes to the institutional root of the resource adequacy problem.

Continuing to add administrative layers to compensate for institutional constraints that could instead be removed is not a sustainable strategy. It is, at best, a bridge. And bridges built without any plan for what comes after them tend to become permanent fixtures.

It is a hopeful sign that these ideas are getting much wider play. In case you missed it, a recent Volts podcast centered on pricing as being better than VPPs for distributed energy resources: https://open.spotify.com/episode/0U0eZ0VBnBuuiDmaqXrWe7?si=A0-FmrndRASwEaVspV3ASg

Imagine the reactions of Zhang Zhigang, State Grid’s CEO, reading this summary.