Electric-Gas Interdependence: History and Transaction Cost Economics

Electric-Gas Interdependence: History and Transaction Cost Economics

Recent winter storms have illuminated the interdependence between electric systems and natural gas systems, an interdependence examined in useful detail in this Canary Media story. Winter Storm Uri in February 2021 was devastating in Texas and other contiguous states to the north, and Winter Storm Elliott on Christmas 2022 strained energy systems from New York state south. In both of these large regional storms, natural gas availability for power plants was an issue, both due to gas production disruptions and gas pipeline transportation and contractual arrangements between power generators and gas suppliers. The Federal Energy Regulatory Commission-North American Electric Corporation final report on the February 2021 freeze identified natural gas disruptions as a major contributing factor, with 58 percent of natural gas generating units experiencing outages during the freeze.

"Natural gas fuel supply issues were caused by natural gas production declines, with 43.3 percent of natural gas production declines caused by freezing temperatures and weather, and 21.5 percent caused by midstream, wellhead or gathering facility power losses, which could be attributed either to rolling blackouts or weather-related outages such as downed power lines."

For the past century and more, the joint policy and operational objectives have been for electric service to be safe (don't get electrocuted), reliable (I flip the switch and the light goes on), and affordable (pretty much everyone can pay their bill comfortably). Over the past decade resilience (system preparation for and rebound from adverse natural and organized threats) and decarbonization (delivering electric service with decreasing amounts of greenhouse gas emissions) have joined the suite of electricity policy objectives. Natural gas production, delivery, and affordability is increasingly part of enabling simultaneous achievement of those objectives (yes, even decarbonization, because as natural gas has fallen in price it has substituted for coal in the generation portfolio).

But it hasn't always been this way. A little history (courtesy of the American Public Gas Association and Direct Energy) and exploration of what transaction cost economics implies can give us some insights into the newly-prominent interdependence between natural gas as an input into electricity. Transaction costs in the supply of gas to power plants are definitely an element in this growing issue.

A Condensed Gas Industry History

People have used natural gas (which is methane) seeps for millennia. In the 18th century in Britain, inventor William Murdoch led the commercialization of gas synthesized from coal (usually known as "town gas"), which was first used for street lighting. Gas lighting in premises grew in the UK and the US in the 19th century as a lighting substitute for expensive whale oil lanterns and inferior candles, before the distillation of kerosene and the invention of the kerosene lantern, and well before commercial electric lighting. Gas was used primarily for lighting until the late 19th century when a chain of inventions enabled its use for building heating and for industrial production. The first use of natural gas for electricity generation did not occur until the late 1930s, by which time gas production and pipeline construction had taken place for several decades, historically contingent on its use in lighting, building heating, and industrial production.

One of my favorite journal articles, Davis & Kilian (2011), recounts the mid-century growth of the natural gas industry and the first federal regulatory forays into the industry:

[Until the shale fracking revolution of the 2000s, m]ost natural gas in the United States is produced in gas fields concentrated in Texas, Louisiana, New Mexico, and Oklahoma and transported by pipeline to gas consumers in the Midwest and Northeast. The traditional problem in the U.S. natural gas industry in the 1930s and 1940s had been one of overproduction. This situation changed in the 1950s. As the domestic pipeline system expanded, supply could barely keep up with rising demand for natural gas among urban consumers in the Midwest and Northeast. Prices increased, much to the dismay of consumer advocates, and pressures arose to regulate interstate sales of natural gas, culminating in a 1954 Supreme Court decision that imposed federal price controls on natural gas sold in the interstate market. Because federal jurisdiction extended only to interstate sales of natural gas, natural gas markets in gas-producing states were left unregulated.

Those urban consumers in the Midwest and Northeast were primarily using natural gas for building heating, sold to them through their regulated utility LDC (local distribution company). The price ceiling imposed in 1954 both increased quantity demanded and decreased quantity supplied, as they do, and by the 1970s the shortages were leading to industrial customer curtailment as well as new home construction substituting into (very inefficient in cold climates and polluting) electric heating instead of gas heating.

The various stages in the natural gas supply chain – production, gathering, storage, pipeline transportation, local distribution – were transacted mostly through a combination of long-term contracts and a little vertical integration. Typically in the US the producer focused on gas field production, and the pipeline owner had long-term contracts with producers as well as supply contracts with LDCs, so the pipeline owner took on price risk; some pipelines were merchant and some also owned production and were vertically integrated, but most pipelines were merchant and took ownership of the gas that they then sold on to LDCs. Pipelines crossing state lines were regulated by the Federal Power Commission (FERC's predecessor) under the Natural Gas Act of 1938's "just and reasonable" interstate commerce standard. The Natural Gas Policy Act of 1978 started a slow deregulatory process that culminated in FERC Orders 436/636 in the early 1990s; a large component of the 436/636 deregulation was the unbundling of natural gas energy sales from natural gas pipeline transportation sales, so now the counterparty to the gas producer in its contracts was no longer the pipeline, but instead the LDC or other purchaser. Post-636 pipelines were legally treated as common carriers and the transportation rates they charged to producers are still regulated using FERC's "just and reasonable" interstate commerce standard. Natural gas price ceilings were removed in 1989.

This potted history of the US natural gas industry in the 20th century does two things that I want to emphasize: it illustrates that for most of the industry's history, power generators were not its customers, and that even within the industry itself, parties used long-term contracts rather than vertical integration to coordinate and to ensure supply reliability. That is a topic I want to dig in to more, but for now let's focus on the growing use of natural gas for electricity generation following the gas price deregulation in 1989 and the restructuring that FERC 436/636 brought about. Another prong of federal regulatory restructuring arose from the Energy Policy Act of 1992. The National Conference of State Legislatures has a good summary of what was an incredibly complicated period of energy policy history:

The idea behind the shift toward shared infrastructure and the economic dispatch of the lowest-cost generation dates back to before the Great Depression. In 1927, three utilities in Pennsylvania, New Jersey and Maryland region formed the PJM power pool . These utilities relinquished some control over their individual systems and generation resources, allowing a common grid operator to manage transmission and generation to optimize economic dispatch. Over the ensuing decades, four additional power pools formed across the country.

However, the traditional utility regulatory structure wasn’t truly altered until the Public Utility Regulatory Policies Act of 1978 (PURPA), which opened the door to independent power producers (IPPs)—non-utility owners and operators of power generating units. Prior to PURPA, these IPPs operated at a competitive disadvantage; utilities didn’t have to consider IPPs in electricity procurement and IPPs weren’t guaranteed access to transmission networks that moved electricity from generators. PURPA required utilities to provide IPPs with an opportunity to participate and compete to supply electricity, but transmission access was still not guaranteed.

The appetite for greater competition in the electric sector grew through the 1980s as advancements in generation technologies made it easier for IPPs to effectively and economically compete with larger, utility-owned power plants. These shifts led Congress to pass the Energy Policy Act of 1992, which aimed to promote wholesale competition in power generation by enabling industry restructuring and removing remaining barriers to competition, including access to transmission. The new law expanded the Federal Energy Regulatory Commission’s (FERC) authority to address these barriers.

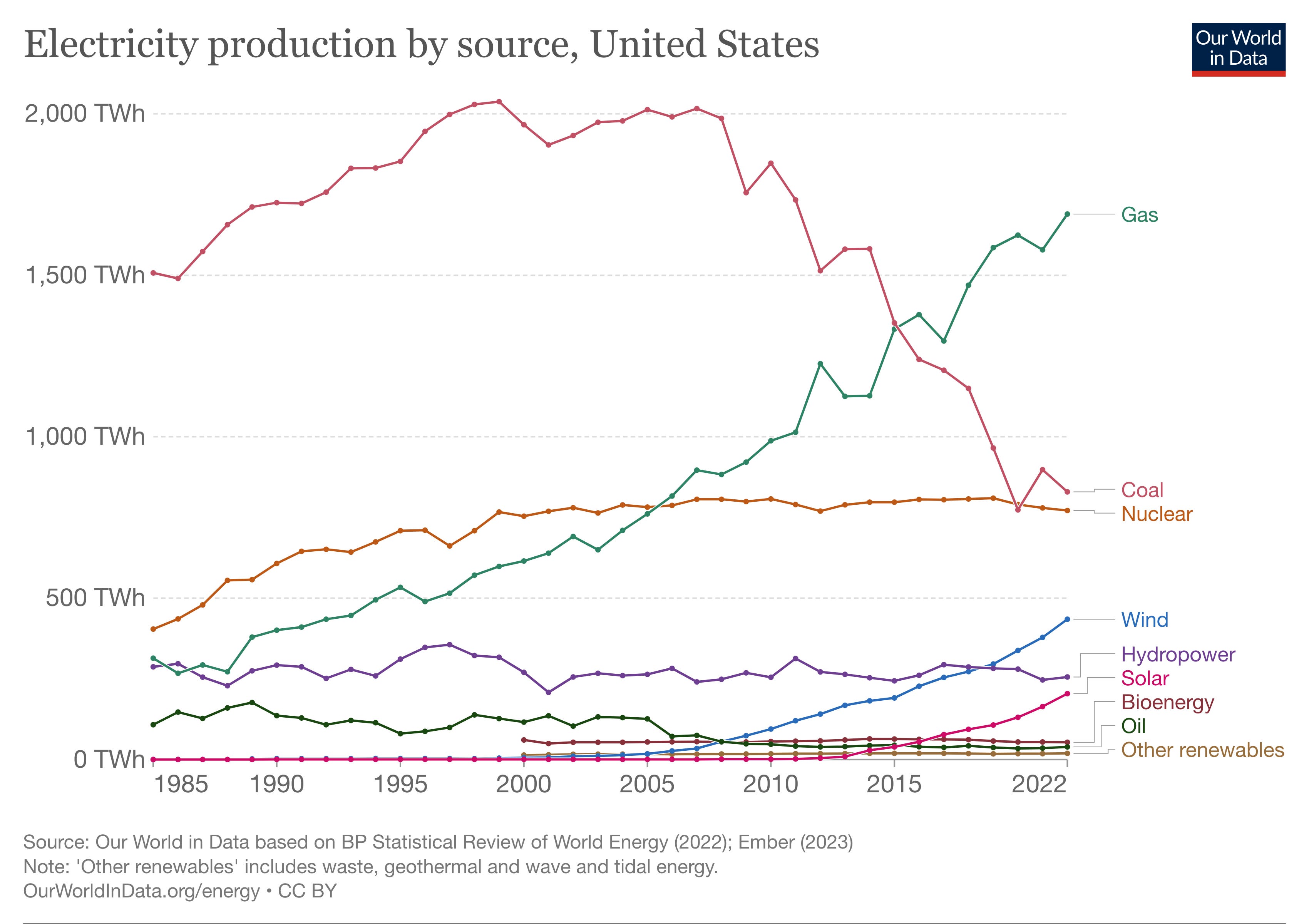

One of those advancements in generation technologies in the 1980s was the combined cycle gas turbine (CCGT) (which if I'm being honest is one of my favorite innovations ever), which could operate economically at smaller scale than a coal or nuclear plant and also was more energy efficient than previous single cycle gas turbines. When combined with the institutional changes wrought by changes in federal regulation, investment in CCGT power plants increased in the 1990s, particularly by independent power producers that entered the new wholesale power markets in the 1990s. Then in the mid-2000s when shale fracking increased the gas supply significantly and lowered prices, the "dash to gas" in electricity generation accelerated. From 1989 onward the increasing use of gas in electricity generation, and in particular its substitution for coal in the 2000s, is apparent.

This growing use of gas has meant more transactions and more contracts (usually long-term) between these two heavily regulated, capital-intensive industries, both of which have complicated supply chains. And the combination of a century of public utility regulation and the organizational culture in each industry has embedded particular operational and business practices, some of which are not entirely compatible with each other. For example, in Winter Storm Elliott the storm occurred on a weekend, and on a long weekend where a major holiday was on a Sunday and was thus observed with a day off for most people on Monday. Power plants and their real-time reliability requirements mean that they have an operational protocol and culture of 24/7 operation, while gas supplier business hours are generally weekdays, so if you run a gas plant and want to secure your gas deliveries for the holiday weekend, you should make that order on Friday morning. But then when the storm rolled in on Christmas Eve, Saturday, the frozen gas wellheads and lines reduced supplies, and the power plant operator who might want to coordinate with the gas folks can't do so because the gas suppliers are out of the office (note that I do not have first hand experience of this phenomenon, but am relying on industry contacts and on presentations at a recent FERC forum on Winter Storm Elliott's aftermath and lessons).

Aligning the real-time electricity requirements with the different operational protocols in gas production requires something to change. Perhaps gas producers invest in more storage, power plant owners invest in more storage, or gas producers change their operations so they have more real-time monitoring, production, and availability. There are also some regulatory responses that have inevitably been suggested, which I suspect will be part of some ongoing research I'm doing, so more on that later.

Transaction Cost Economics Can Help Us Think About This

Aligning different yet interdependent operational cultures to coordinate reliable input supply is hard. One approach is something I alluded to earlier: vertical integration. What if power plant owners bought natural gas producers? The logic from transaction cost economics has two parts: (1) when there are transaction costs that make market exchange a costly way to ensure input supply, buying the input supplier may be a lower-cost way of securing supply; (2) one of those transaction costs may be what's called asset specificity, where the input is very specific to the production process and the input supplier can hold out for a higher price because their input is so important to the downstream production process. Nobel laureate Oliver Williamson was one of the pioneering scholars in the organizational implications of transaction costs, in understanding which transactions occur in markets through contracts and which occur in firms through hierarchical managerial relations. His work on asset specificity and the holdout problem in particular transformed our understanding of vertical integration, why it emerges, and what its benefits are. He also incorporated the costs of vertical integration in his work, including the managerial costs of coordinating different management and operational practices that may be better suited to stand-alone firms than to vertically integrating them. It's all about weighing organizational benefits and costs, evaluating those tradeoffs at the margin.

I'm not recommending that power plants vertically integrate with gas production, but considering the question gives us an opportunity to think systematically about where the institutional pinch points are that are causing problems as electric and gas systems become more interdependent. Taking those two pieces of logic in turn, the existence of transaction costs does not necessarily mean that the only organizational approach to minimizing them is to vertically integrate. The other approach is one that's been in practice for decades within the gas industry and is the standard approach in gas-electric coordination: long-term contracts. One important insight from transaction cost economics is the extent to which long-term contracting is an organizational substitute for vertical integration. Contracts are necessarily incomplete because it's impossible for contracting parties to have perfect foresight, but if they can anticipate the possible conflicts of interest between the parties and problems that can crop up and they can write good enough contingent contracts for a long enough period, that can yield the relationship reliability that both parties want. On the asset specificity point, given the physical characteristics of methane it's hard to argue that Firm A's methane is more customized than Firm B's methane to Power Plant C's production. The asset specificity question is more likely to arise with the pipeline than with the producer, and there the contractual relationship is mediated by FERC pipeline regulations.

The classic reference for this line of inquiry is Klein, Crawford, and Alchian (1978). If I had a "desert island discs" list of top papers I'd take with me to the island, this is one of them, because they lay out the theory for vertical integration and long-term contracting as organizational substitutes and the role that asset specificity may play in which one ends up being adopted (there's been ongoing back-and-forth in the literature on their application to the specific case of General Motors and Fisher Body, but it's still a seminal article). Another important paper in this thread of literature is Monteverde and Teece (1982), applying data from the automobile industry to test the relation of transaction costs to vertical integration.

We can use transaction cost economics to ask why the existing supply contracts aren't yielding the desired outcomes, and to identify where some transaction costs are arising that might not have been relevant or apparent when gas fired generation was smaller or when weather patterns varied in a different distribution. We can also use it to dig more deeply into the roles that regulatory institutions can and do play in creating transaction costs that are then hard to reduce through non-regulatory means. Electric-gas interdependence is not going away, so considering these questions will be important for avoiding future supply disruptions, outages, and deaths.