Market Adaptation to Changing Conditions

It's not time to reconsider uniform price markets in electricity

Evolving Market Design and Resource Adequacy

Today electricity market participants and analysts are paying close attention to Texas, where a heat wave is bringing several days of triple-digit heat and, combined with economic growth and a growing population, is pushing electricity demand to a new forecast all-time high (ERCOT's market dashboard is a good way to get a picture of current conditions in their markets). So far they are under normal operating conditions and are forecast to continue reliable service, but operating margins are tight.

This pattern of stress around summer peaks has been common in electric systems for decades, and system planning and investment have been targeted at meeting those peaks reliably. Summer peaks are known unknowns. Grid operators and market operators perform refined risk modeling to plan for those peaks so that when they occur, sufficient resources are available to meet demand, a criterion known as resource adequacy.

What's new is the variability in that system stress in the winter, with large weather events like Winter Storm Uri in Texas in February 2021 and Winter Storm Elliott in the Mid-Atlantic and South on Christmas 2022. In both of these large storms, gas-fueled power plants were unable to secure gas supplies to enable them to run, leading to outages. Changing weather patterns are revealing unknown unknowns in the electric system, such as the extent to which the interdependence between the electricity industry and the gas industry is a weakness from a resource adequacy perspective, if the risk modeling assumes the gas will be delivered.

One unknown unknown that we've discovered is the extent to which wholesale power market institutions were tuned to the 1990s policy objectives and the 1990s generation technologies, and the changing environment has had resource adequacy implications. In the 1990s, technological change and cost overruns from regulated utilities led to regulatory restructuring and the creation of regional wholesale power markets, the history of which I discussed in my recent newsletter on Texas.

The State Senate is Messing with Texas

We need to talk about Texas. The Texas electricity model, that is – its promise as a fully unbundled, competitive system, its performance during winter stresses like Winter Storm Uri in 2021, and how the Texas legislature is politicizing markets through its attempts to "reform" them by subsidizing natural gas generation and raising costs on renewables.

The pressing issues of the 1990s, particularly cost overruns, lack of affordability, and operating inefficiency arising from failures of regulation led to a focus on competition among power producers as a flexible and adaptable approach to improving productivity and capacity utilization, reducing generation costs, and having those benefits all flow through to consumers through lower retail rates. The primary mechanism for that evolution over time was dynamic investment incentives in the form of market prices to invest in more productive and efficient technologies. But we're learning through experience that these market designs are not as robust to changing power technologies and changing policy environments as we want in order to achieve both economic efficiency and resource adequacy. Wholesale power market operators (regional transmission organizations or RTOs) are working to adapt to these changes, with mixed success, as the consequences of Uri and Elliott revealed.

Which brings us to the current widespread discussions of "what to do" in this complicated and changing context. Yesterday the Federal Energy Regulatory Commission (FERC) held a PJM Capacity Market Forum to discuss these matters in depth in the context of the PJM Interconnection's proposed changes to its market design and to its risk modeling to improve resource adequacy. In May the Energy Law Journal published an article on changing market designs and resource adequacy from FERC Commissioner Mark Christie, It's Time To Reconsider Single-Clearing Price Mechanisms In U.S. Energy Markets. In his article he raised some important, valid points, but through flawed economic analysis came to unsupportable conclusions. His focus on some aspects of market design and not others fails to get at the root cause of why these market designs are not adapting to the resource adequacy challenges of the 2020s.

What To Do: Change Auction Clearing Price Rule?

Commissioner Christie addressed several issues that are challenging existing wholesale power markets, focusing on three: specific aspects of the market designs themselves, the extent to which electricity markets are not "true" markets, and exogenous policy factors like subsidies and generation portfolio regulations from state and federal governments that benefit some technologies. Today I want to focus on his market design criticisms, and will defer the other discussions to the future.

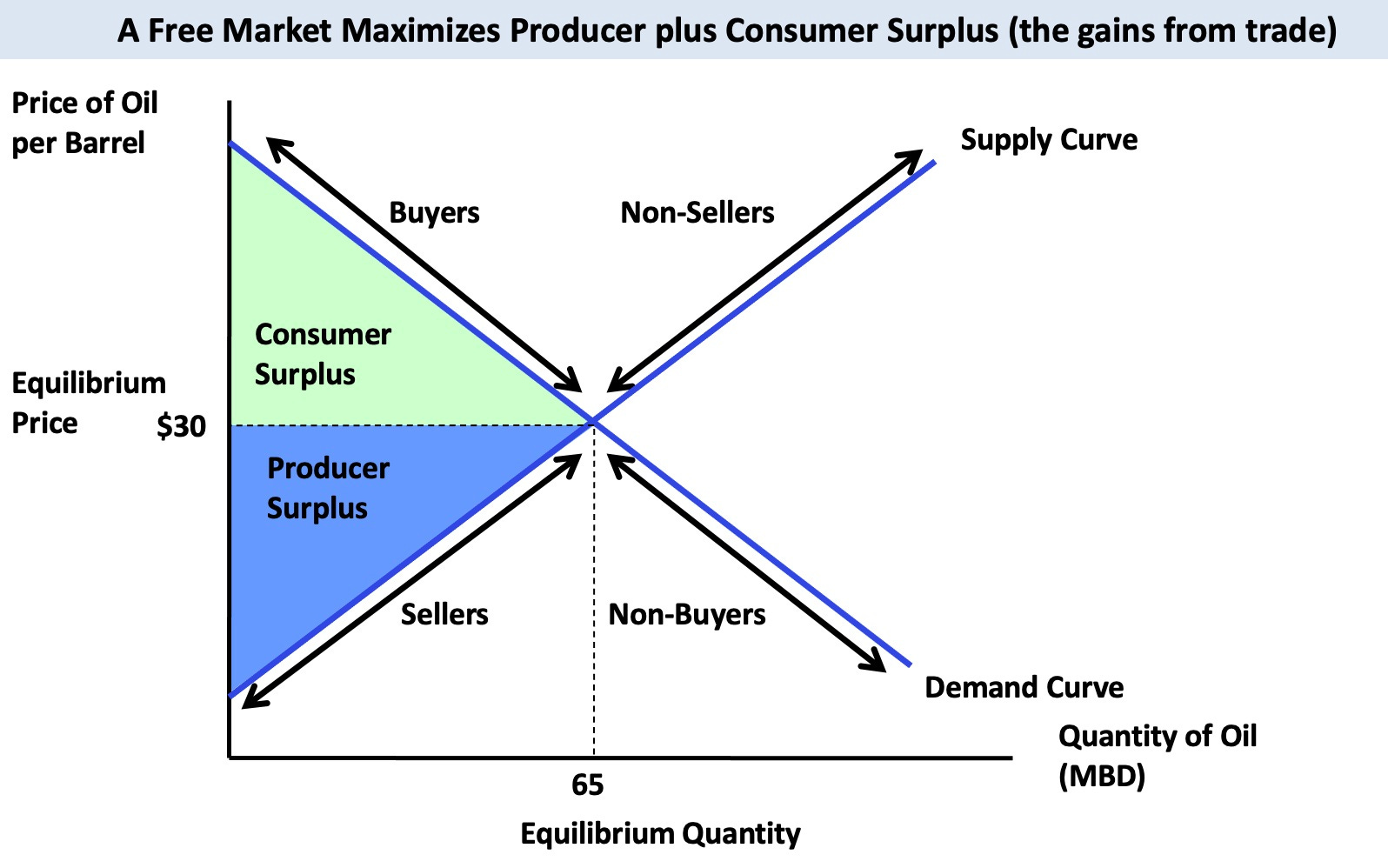

Christie's criticisms of wholesale power market design focus on one specific dimension, the settlement rule in each market period. Power markets are auctions, and are a particular form of auction called a uniform price auction (Christie calls them single clearing price or SCP markets). In a uniform price auction all sellers who offer at the market clearing price or lower receive the market clearing price, and all buyers pay the market clearing price. The market clearing price simultaneously communicates the marginal value of the last buyer and the marginal cost of the last seller. The value creation or gains from trade in the market period is the sum of consumer surplus (what the buyers were willing to pay but didn't have to) and producer surplus (what the sellers receive above their marginal cost). That surplus represents the static welfare effects of market exchange – given a set of resources and a set of buyers with preferences, the market supply and demand in combination (remember it's supply AND demand) provide an informationally parsimonious mechanism for allocating those resources from those who can produce most cheaply to those who value the good the most at that time.

Supply AND Demand

This post is an ode to consumer demand and its importance to determining value in electricity. In Book V, Chapter II, paragraph 7 of his seminal Principles of Economics in 1890, economist Alfred Marshall described the market interaction between supply and demand as two blades of a pair of scissors.

Sure, static resource allocation is great, and has been one of the considerable benefits of the move from regulated vertical integration to (regulated) wholesale markets. But the real value creation potential is in the dynamics, the use of those market clearing prices to determine which sellers produce as demand changes over time (in electricity this is called security constrained economic dispatch). Power markets do not yet take full advantage of the flexibility that's possible with better mechanisms for making demand more active in these markets, which are not really double auctions. Yet, compared to the consumption and dispatch decisions that take place in the absence of market processes (i.e., in a regulatory process), markets enable more flexibility and more adaptability over time as circumstances change. In the face of growing uncertainty, that flexibility and adaptability will be essential elements of maintaining resource adequacy.

Source: Cowen & Tabarrok (2021)

The dynamics in markets provide another important element of resource adequacy: investment incentives. Opening wholesale power markets in the 1990s communicated those dynamics to new power producers interested in profiting from improved productivity and higher capacity utilization at lower operating costs, and communicated those dynamics in time scales and in decentralized contexts that regulated vertical integration could never have achieved. In the 1990s, even before the fracking boom post-2008 lowered gas prices, those incentives all pointed to the then-new combined-cycle gas turbine (one of the best inventions of the 20th century!). The "dash to gas" delivered on the policy objectives underlying restructuring at the time, and also delivered substantial greenhouse gas reductions because gas mostly substituted for coal in the generation mix. Again, the relevant comparison is to a regulated resource planning process, which is likely to be slower and

One important historical note that is underappreciated today: the gas extraction, pipeline, and distribution systems were not built for gas generation of electricity. The gas industry grew up as an industry for building heating and water heating, then grew in industrial use. Until the 1970s it was largely illegal to use gas for electricity generation, so it shouldn't be surprising that the gas infrastructure strains to meet the growing demands for electricity generation, and that the culture of the gas industry is not attuned to its interdependence as a vital input in electricity. But that's a topic for another day ...

Uniform price auctions have a long and deep history both in theory and in practice in many industries for creating most of the possible static and dynamic value in markets. They have three important properties that Commissioner Christie overlooks in his criticism: dynamic incentives, strategic incentives, and ease of implementation. That triangle of producer surplus that the low-cost suppliers receive does two important things – it allows that seller to earn some revenue to cover their fixed costs and thus gives them an incentive to bid their true marginal cost instead of some higher average bid, and it provides higher profits to lower-cost sellers, which provides greater incentives to invest in more lower-cost production technologies. From an efficiency perspective, this is solid gold. In terms of strategic incentives (getting in to game theory and mechanism design), it's a market design that gives sellers incentives to bid their true marginal cost, and in combination with the rivalry with other sellers, that creates high-powered incentives to bid their marginal cost. This is why in the early days so many economists paid so much attention to concentration and market power, which undermines the important strategic incentives of the uniform price auction. Finally, in many ways it's easier to implement and communicate to all market participants, and in these complicated settings ease of understanding and implementation really matters.

For these reasons Commissioner Christie's criticism of uniform price auctions as leading to higher prices is misguided. He advocates instead moving to a discriminatory or pay-as-bid auction design, in which sellers receive the actual bids that they submit rather than the market clearing price, and he does so because he argues that the discriminatory auction will deliver more cost savings to consumers (p. 3). Discriminatory auctions fail to deliver the dynamic, strategic, and implementation benefits of uniform price auctions. In a discriminatory auction sellers receive only their offer, which drastically reduces their producer surplus unless they submit bids that are well above their true marginal cost, so the investment incentives are muddied and poorly communicated. That's especially true given that there is still seller rivalry, so they have incentives to overstate their costs in their offers but are still competing with each other. And in a discriminatory auction, how does the market platform determine what prices the buyers pay? It starts to look more like over-the-counter and bilateral contracting and gets costlier to implement.

The large literature on comparing these two market designs suggests that the discriminatory auction has no strong welfare benefits over the uniform price auction. Back in the late 1990s similar criticisms of uniform price electricity markets led to considerable research, summarized by Natalia Fabra et al. (2002) as finding that in some ways discriminatory auctions weakly outperform uniform price auctions, and vice versa.

It is well-known among auction theorists that discriminatory auctions are not generally superior to uniform auctions. Both types of auction are commonly used in financial and other markets, and there is now a voluminous economic literature devoted to their study. In multi-unit settings the comparison between these two auction forms is particularly complex. Neither theory nor empirical evidence tell us that discriminatory auctions perform better than uniform auctions in markets such as those for electricity, although this has now become controversial.

In laboratory experiments, Bower and Bunn (2001) found that "The discriminatory auction results in higher market prices than the uniform-price auction. This is because market prices are not publicly available and agents with a large market share gain a significant informational advantage in a discriminatory auction, thereby facing less competitive pressure." Rassenti, Smith, and Wilson (2003) found in their experimental analysis that

A “pay-as-offered” or discriminatory price auction (DPA) has been proposed to solve the problem of inflated and volatile wholesale electricity prices. Using the experimental method we compare the DPA with a uniform price auction (UPA), strictly controlling for unilateral market power. We find that a DPA indeed substantially reduces price volatility. However, in a no market power design, prices in a DPA converge to the high prices of a uniform price auction with structural market power. That is, the DPA in a no market power environment is as anti-competitive as a UPA with structurally introduced market power.

There are flaws in existing market designs that have hampered resource adequacy, but eliminating the uniform price market design in favor of a discriminatory price auction is not going to remedy those flaws. Uniform price markets markets enable flexibility and adaptability, as well as dynamic efficiency through clear investment incentives. Commissioner Christie's analysis does not incorporate those benefits.

It's time to reconsider how wholesale power market designs can adapt better to the changing technological, economic, and policy environments in which they operate to enable affordability and resource adequacy, and I'll have more to say on that subject. It's not time to reconsider uniform clearing price market designs.

I can’t wait for the next installment!

Great article! As an energy economist, do you have a preference between wholesale market centric designs like ERCOT and Australia, or wholesale market + capacity payments like PJM?